Banking experts say they won't be the last. At least 50 of the country's more than 5,000 banks are considered troubled, according to Bauer Financia

Banking experts say they won’t be the last.

At least 50 of the country’s more than 5,000 banks are considered troubled, according to Bauer Financial, a company in Coral Gables, Florida, that tracks the health of financial institutions.

That means they have high levels of nonperforming loans and not enough capital set aside to protect them if more of their loans go bad or if the economy gets any worse.

The most troubled banks have high levels of bad loans and other assets compared with their total capital on hand, a measure known as a “Texas Ratio” and one of the most important indicators used by analysts to determine a bank’s long-term viability.

Not all of these banks will fail, experts say, and there’s plenty of disagreement as to how many will go under before the Covid-19-related crisis comes to an end.

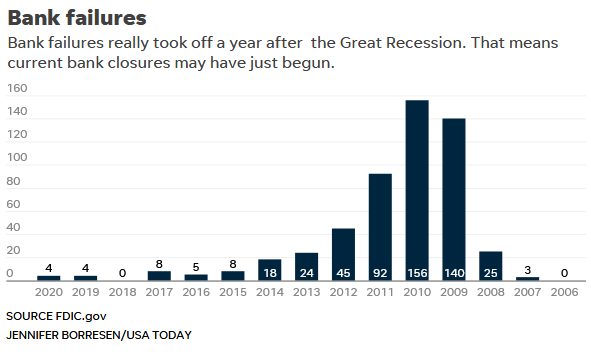

“I’d say 10 or less,” says Christopher Marinac, banking analyst and director of research with Janney Montgomery Scott LLC, a financial advisory firm in Atlanta. “And a lot of these banks will be small.” So it will be a lot different from 2008 though 2012 when nearly 500 banks failed.

But Jason Vanslette, a mortgage foreclosure specialist and partner at Kelley Kronenberg law firm, is more pessimistic.

From vacant storefronts and office buildings to renters’ inability to pay rent due to financial hardship, he sees the pandemic taking a much greater toll on the economy – one that will result in far more foreclosures, bankruptcies and bank failures than many think.

“We’re gearing up for what could be close to a 2008 housing crisis,” Vanslette said. “And commercial loans, my God. There’s going to be a massive amount of defaults on commercial properties.”

Hotel and retail loans are already going bad in record numbers, and office loans could be the next shoe to drop, Vanslette said. A lot of small businesses are still struggling, especially in areas of the country that depend on tourism or the oil and gas industry.

“It could take 12 to 18 months before we get a real idea of the damage,” Vanslette said.

Two struggling banks

Besides being tiny, the two banks that failed in October have little in common.

First City Bank of Florida in Fort Walton Beach, with its $135 million in assets, had been struggling with problem loans since the last recession. Having to set aside additional capital for loan loss provisions to deal with Covid related problems simply pushed it over the edge.

Almena State Bank, with $70 million in assets, was different. The Kansas bank got hit hard by bad agricultural loans made during the past few years of falling commodity prices brought on by robust harvests and the US-China trade war.

Of the 10 banks considered most troubled by Bauer Financial, six have similar stories to that of First City. They have been weighted down by loan problems for more than 10 years.

The other four are more like Almena – impacted by the flagging economy in farm states, where agricultural loan delinquencies hit an eight-year high in March and repayment rates have continued declining until this summer, according the Federal Reserve of Kansas City.

Two of the most troubled banks were also upended by fraud on the part of their chief executive officers.

Mary Beyer Halsey, the former CEO of Cecil Bank in Elkton, Maryland, pleaded guilty in July to multiple federal charges, including bank fraud, in a real estate scheme that cost the bank to lose about $145,000.

Halsey has been gone from the bank since 2013, but she was sentenced to two years in prison earlier this month.

Meanwhile, It was only a year and half ago that Aaron Johnson stepped down from his position as CEO of Farmers Bank in Carnegie, Oklahoma, after getting sued by three shareholders who claimed he fraudulently sold them $1.5 million in bank stock that had already been pledged as collateral to secure another loan.

Both Cecil Bank and Farmers Bank, which had the highest Texas Ratios in the country as of the end of June, are now under new management and executives are confident that they will make it through this rocky period.

“We have all new shareholders and fresh capital,” said Clint Stone, the new CEO of Farmers Bank. But he declined to say how much the bank raised.

“It will be in our December call report,” Stone said, referring to the periodic reports on financial health that banks must file with regulators.

Terrie Spiro, the president and CEO of Cecil Bank, was more expansive.

In charge of the bank since Halsey’s departure in late 2013, Spiro said she’s fought long and hard to rid Cecil Bank of problem loans built up during the real estate boom in the mid-2000s. And while Cecil Bank’s Texas Ratio may look high at around 180%, Spiro said it’s a lot lower now than it was in 2017 before a $30 million capital infusion.

“Just on the eve of getting that money our Texas Ratio was 998%,” Spiro said. “Working in a bank in that situation is akin to being an emergency room doctor and making sure your patient doesn’t die on the table.”

Spiro acknowledged that Covid has put additional stress on community banks. That’s because they’re not as diversified as big banks, she said. They’re more dependent on commercial real estate and small business loans that have been hit hard by the crisis.

Spiro added that banks have no problem getting deposits, but there’s not a lot of profitable places to invest those deposits at the moment, Bonds and securities aren’t paying much interest and demand for loans is minimal.

But Cecil Bank still has real estate that it has been selling off at a profit and its Texas Ratio is moving in the right direction.

“It’s the lowest it’s been since I’ve been here,” Spiro said.

Weathering the storm

Other bankers whose institutions are at the top of Bauer’s troubled list also expressed optimism in the face of difficult times.

Evelyn Smalls, the president and CEO of United Bank of Philadelphia, said that fresh capital in the third quarter has enabled her bank to reduce its Texas Ratio from 125% to 74%.

Founded in 1992, the bank is one of dozens of black-owned financial institutions in the country. It is focused on making business loans in the inner city and has often received capital infusions from the local government, including $3.5 million from the City of Philadelphia and $1.5 million from the Philadelphia Industrial Development Corp.in May 2019.

Smalls said loans to daycare centers have been a particular sweet spot in terms of pandemic lending as health care and other essential workers have been desperate for a safe place for their kids.

“We feel we can weather the storm,” Smalls said.

Community Bank & Trust CEO William Stump Jr. feels the same way.

His Lagrange, Georgia, bank had the third-highest Texas Ratio in the country at the end of June. But Stump said plans are underway to sell off his holding company’s Alabama bank and to raise $7 million in fresh capital – moves that will increase Tier 1 capital to nearly $16 million.

“After more than 10 years of playing defense (unwinding bad loans and selling off real estate), we’ll be back on offense again,” Stump said.

With regard to Covid, Slump said he hasn’t seen a big rise in bad loans, and that the economy in his area of Georgia remains fairly strong.

At Nantahala Bank & Trust in Franklin, North Carolina, CEO Tim Hubbs said the Covid pandemic had actually benefitted his bank, which has suffered from a hangover of bad loans since the Great Recession.

Located in the mountains near Asheville, Franklin has been attracting an influx of people wanting to migrate permanently from big cities and tourists just looking for a break,

“People having been buying property and our pipeline for new loans has grown,” Hubbs said. “We don’t have enough housing and we’ve sold a lot of our outstanding real estate.”

Bank failures depend on recovery

Matt Anderson, managing director of Trepp LLC, which tracks commercial real estate markets, said the ultimate number of bank failures will depend on whether the economy continues to recover.

One good sign, he said, is that banks did not set aside as much money in their loan loss reserves in the third quarter as they did in the first two quarters of the year, which means that they see loan problems as manageable.

But Anderson said another indicator of how well banks are doing will come at the end of the fourth quarter. That’s because the CARES Act permitted banks to postpone classifying loans as overdue for 180 days, and that 180 days is up in the fourth quarter.

“Banks have treated those loans as if they were still performing,” Anderson said, “By our estimates, 70% of hotel loans have gotten deferrals and 40% to 50% of retail properties have gotten deferrals.”

The office sector is another mystery, Anderson said. It is unclear how many owners of office space will default on loans if and when tenants decide not to renew leases.

“There’s a lot of sublease space that’s being put on the market,” Anderson said. “For owners, that’s the worst thing being put out there because people subleasing space are just trying to reduce their losses. They’re not trying to make money. So that has a depressing effect on rents.”

Then there’s small businesses.

“They have much less access to capital and we’ve already seen a wave of small businesses shutting down,” Anderson said. “If we have another wave of small businesses going under, it will put pressure on banks.”

Source : eu.usatoday.com